RBI Regulatory Framework[1]

RBI has always come up with a regulatory framework in the past, in order to keep up with the dynamic market as the NBFC sector has evolved in terms of size, operations, technological and sophistication. Since 2006, RBI has introduced differential regulation linked to size, in a limited manner. RBI, to re-examine the suitability of the regulatory approach, there is a need for re-orientation. Within the universe of systematically important NBFCs, an additional identifier has been placed at ₹ 5000 crores. Within which additional regulations are made applicable to large NBFCs, as, disenthralled growth out of the liberal regulatory framework, within an interconnected financial system can lead to systematic risk. Failure in large and deeply interconnected NBFCs can lead to shocks rippling to the financial sector including small and mid-sized NBFCs.

Using the principle of proportionality, which expounds that degree of regulation of a financial entity should be commensurate with the perception of risk the entity poses to the financial system, the scale of its operation. Inspired by the

1. G-SIBs, developed by BCBS

2. G-SIIs, developed by IAIS

3. NBNI G-SIFIs, developed jointly by FSB and IOSCA

3 triggers are used for triggering the rule of proportionality:

1. Comprehensive Risk perception: When NBFC crosses a threshold for identified parameters (size, leverage, interconnectedness, complexity, and supervisory inputs), it is subject to proportionately higher regulations.

2. Size of operations: If the balance sheet of an NBFC exceeds a threshold, it can be regulated on a higher pedestal.

3. The activity of NBFC: Certain NBFCs are unlikely to pose risk, hence can be regulated lightly. Type 1 NBFCs, do not have access to public funds and customer interface, as they function from their funds, thus their risk posing ability is low. Also, NBFC P2P lending platforms, NBFC – AA, and NOFHC (Bank Holding Company), do not pose any risk to credit intermediation. There are some NBFCs such as NBFC-HFC, IFC, IDF SPD, and CIC, which have some impact on the systematic domain.

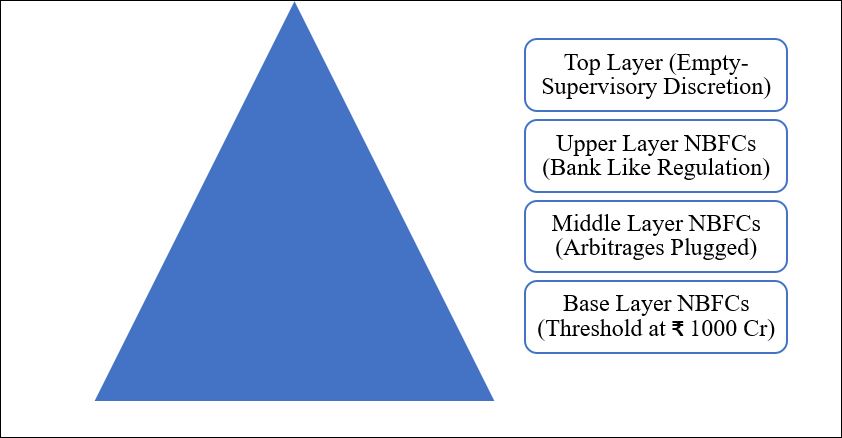

Scale Based Framework

A regulatory framework to solve the above problems and to address them efficiently in the dynamic market ecosystem, based on proportionality can be introduced. The framework, if visualized graphically or pictographically, can be visualized as a pyramid.

NBFC – BL (The Bottom / Base Layer)

This layer would have the least regulatory intervention. The layer would consist of about 9,209 NBFCs, currently classified as non-systematically important NBFCs (NBFC-ND), NBFC-P2P lending platforms (Peer to Peer), NBFC-AA (Account Aggregators), NOFHC (Non-Operative Financial Holding Company), and Type 1 NBFCs up to Rs 1000 Crores asset size. With the objective of strengthening the entry-level norms, based on the increase in prices, real GDP, and regulatory judgment, the entry point norms will be revised from ₹ 2 Crore to ₹ 20 Crores. The extant NPA ( Non-Performing Assets) classification norm will be harmonized which was earlier of 180 days would be now of 90 days as business cycle aspects of NBFC clients often demand relaxed norms because their cash flows are uniquely different and longer in frequency.

The Mid Layer

The regulatory regime would be stricter than the previous one. Adverse Regulatory arbitrage vis-à-vis banks can be addressed for NBFCs, with the objective to reduce systematic risk spill-overs.

This layer would contain NBFCs currently classified as systematically important NBFCs (NBFC-ND-SI), deposit-taking NBFCs (NBFC-D), HFCs (Housing Finance Companies), IFCs (Infrastructure Finance Companies), IDFs (Infrastructure Debt Funds), SPDs (Standalone Primary Dealers), and CICs (Core Investment Companies). The linkage of their exposure limits is to be changed from Owned funds to Tier I capital, which is currently applicable to banks. The extant credit concentration limits prescribed for NBFC ML for their lending and investment can be merged into one exposure limit which is 25% for a single borrower and 40% for a group of borrowers.

IPO Financing

Emphasizing that Initial Public Offer financing by NBFCs has come under critical observation, for the reason of their abuse of the system. The paper has proposed to fix a ceiling of ₹ 1 crore per individual for any NBFC. Sub limit within commercial real estate exposure ceiling should be fixed internally for financing the land acquisition.

Lending Restrictions

The restriction put can be not allowing the companies to take loans and to provide them with the same for buying back of shares / Securities. NBFCs with ten and more branches shall mandatorily be required to adopt Core Banking Solution. A uniform tenure of three consecutive years will be applicable for statutory auditors of the NBFC. Compensation guidelines for NBFCs along the lines of banks can be considered to address issues arising out of excessive risk-taking caused by misaligned compensation packages. The disclosures which are applicable to the banks would be used for NBFCs which would increase transparency and understanding of the entity.

The Upper Layer

This Layer would contain the NBFCs which have a huge potential of systematic spill-over of risks and they have the ability to change and influence the financial stability. The regulations in this layer would be Bank-like.

The Identification of the upper layer NBFCs

In order to include an NBFC and to be recognized as NBFC-UL, a two-phase parametric analysis, quantitative and qualitative / Supervisory inputs would be carried out. The quantitative parameters will have 70% weightage and qualitative parameters / supervisory inputs will be having 30%.

The Quantitative Parameter (70%) would be:

1. Size and Leverage | 30 Parameter Weights (PW)

2. Interconnectedness | 25 PW

3. Complexity | 10 PW

4. Nature and Type of Liabilities | 10 PW

5. Group Structure | 10 PW

6. Segment Penetration | 10 PW

TOTAL: 100 PW

Capital Regulations under the framework of NBFC UL

Capital Requirements: CET (Common Entity Tier) 1 capital could be introduced for NBFC – UL with the objective of enhancing the quality of the working capital. CET 1 may be prescribed at 9 percent within the Tier 1 capital.

Standard Asset Provisioning: In order to tune the regulatory framework for NBFC UL to greater sensitivity, NBFC should be prescribed differential standard asset provisioning on banks’ lines.

The regulatory tools can be calibrated on the lines of Private banks, which means that NBFCs should be subject to the mandatory listing requirement and should follow consequent Listing Obligations and Disclosure Requirements.

NBFCs have seen phenomenal growth, from 12% on the balance sheets of the banks to more than a quarter of the size of banks. This will also impact fintech players who collaborate / partner with NBFCs. NBFCs could have stronger vigilance over their partners and service providers. The guidelines will provide more confidence to potential investors of the ecosystem. They are expected to improve the funding conditions of the sector by strengthening risk controls and frameworks and preserving the Non-Banking Financial Institutions. The resilience to credit shocks would increase and be conditioned in the companies.

[1] Discussion paper on Revised Regulatory Framework- a Scale Based Approach (rbi.org.in)

Image Source

Author: Saptak Pandya